Spain white shirt

Spain white shirt About the different perspectives on the European economy these days have circulated both by the BEA as large media positions have been found: wishful thinking, moderate bitter and pessimistic. Whereas one of the main articles comes precisely from a Nobel Prize ( Paul Krugman in the New York Times ) I guess these lines can only be considered as a contribution to unraveling the general confusion. A confession from ...

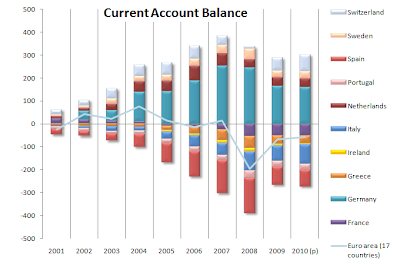

Since the formation of the Euro block some countries (Italy, Ireland, Greece, Spain, Portugal ...) had a current account deficit, in many cases growing. After the international crisis, these countries faced a decline the price of real estate which, added to the contraction in world trade, strongly affected the affordability of a wide range of actors including public sector (in this situation and similar ones in the story we referred to here ) . In this context, the inability to obtain financing required a correction of current account results. Correct this imbalance in turn required a change in relative prices. In that case, why do not devalue?

Far away and long ago Argentina's economy had, after the implementation of the scheme convertibility, successive current account deficits. Tells the story (probably apocryphal) that a reviled but reminded Finance Minister against the tribulations of his interlocutor on this point retorted "This is not a current account deficit is a capital account surplus."

Beyond the rhetorical elegance of former minister, the fact is that by definition all current account deficit has as its counterpart funding from other countries, ie a surplus of capital account. Trivial. When you remember the benefits of financial integration European countries tends to be emphasized that the decline in rates meant for the less developed members of the single currency. But, in principle, the other members of the euro area, particularly Germany, but also the Netherlands, Switzerland and Sweden, had access to a vast market where to channel their excess savings. Ultimately, the development strategy of "export led" allowed these countries to grow through trade with its partners, financial institutions exported while the domestic savings surplus capital. In plain language, while over the counter the more developed European countries offering goods to other partners through the single market, the new financial integration to extend no-fault allowed the grocer's account (and with low transaction costs!). Authentic happiness chain: while some grew through consumption (including construction financing) the others did for the external sector. The crisis broke off the romance.

devalue in this context does not alter the balance of forces and would therefore be safe and is that bad though, Europe's problem is internal to Europe. The future will depend on the possibility that this group of countries to define a new framework for joint development with no winners or losers. This is important because the burden of adjustment should fall not only in economies that increased their borrowing in recent years, but also those who fund it (accepting that part of that loan was given was wrong).

In this context, less developed countries seek an internal devaluation through deflation. As you rightly mentioned Krugman, this must necessarily be accompanied by a restructuring (how often removed?) In public and private debt, as price decreases with an inflexible debt could lead to a collapse of the payment chain. The position of developed countries in this context is striking: to demand payment of the debt requires a reversal of the balance, at least, the trade balance, which would run counter to its own development policy. These contradictions do not seem to have a simple resolution in the Euro.

Optimists and pessimists do not seem to reach convincing arguments. Optimists should be able to show a historical example of a successful disinflation, or at least, establish the characteristics that distinguish this from other deflations. The argument about the impossibility of the collapse of Euro based on exit costs and the historical inevitability of the "united Europe" (the mosaic of languages \u200b\u200band customs with little in common) seem inadequate. As a good South American (or rather, Argentina), I guess I'm closer to the pessimism, or at least prepared for the worst. But the possibility of defining the sequence of events that predict the coming of the apocalypse seems closer to futurology than the economy.

0 comments:

Post a Comment